Imran Bhatti

The metaphor of a “love triangle” works because it captures what formal diplomatic language often hides: global politics is rarely about loyalty alone. It is about leverage, timing, and the ability to keep more than one powerful partner invested in you at the same time. The United Arab Emirates’ decision to leave OPEC does not simply mark an institutional rupture in oil politics; it completes a triangular structure that has been emerging for years — one in which Abu Dhabi is no longer just a disciplined member of a Saudi-led producers’ club, but an agile power balancing between Riyadh’s regional weight, Washington’s security architecture, and Asia’s demand-driven economic future, especially China and India.

To grasp the significance of the move, one must begin with OPEC’s original purpose. Founded in 1960 by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela, OPEC was designed to coordinate petroleum policies, secure fair and stable prices for producers, ensure regular supply for consumers, and provide a fair return on investment in the industry. The UAE joined in 1967, initially through Abu Dhabi, long before the federation formally emerged in 1971. In other words, Emirati oil policy was woven into OPEC’s institutional DNA for nearly six decades.

That is precisely why the exit matters. Reuters reports that the UAE will leave on May 1, with Energy Minister Suhail al-Mazrouei describing the decision as a strategic policy choice taken after reviewing current and future production policy. The move weakens OPEC’s control over global supply, especially because the UAE is one of the few members, alongside Saudi Arabia, with meaningful spare capacity. This is not Angola or Ecuador departing from the margins. This is a core producer with the technical and financial ability to reshape market outcomes once geopolitical constraints ease.

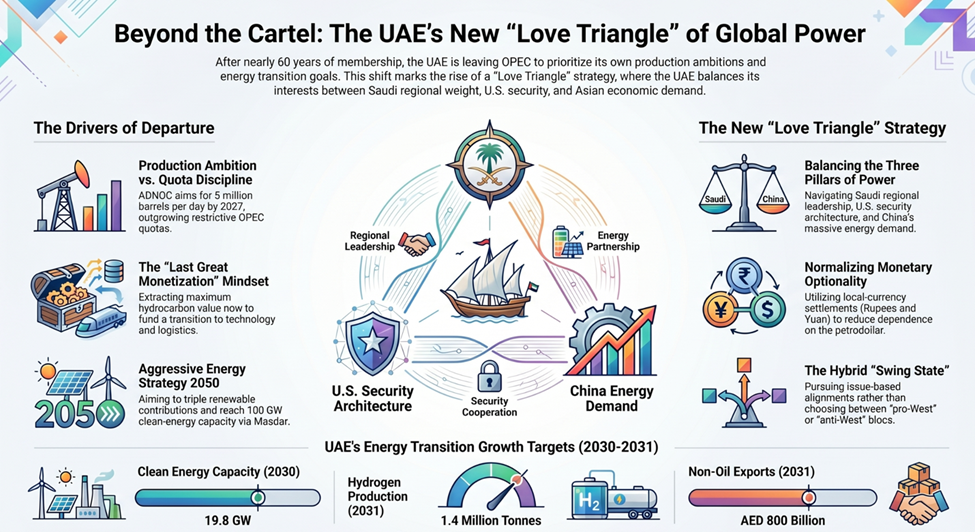

At one level, the reason is straightforward: production ambition and quota discipline had become increasingly incompatible. ADNOC has been explicit about its objective to raise lower-carbon oil production capacity to 5 million barrels per day by 2027. For a country that has spent heavily to expand upstream capacity, remaining tied to a quota framework that limits monetization of that capacity makes progressively less strategic sense. In plain terms, Abu Dhabi no longer wanted to invest like a growth producer while behaving like a constrained cartel member.

But there is a deeper logic at work. The UAE appears to be acting from a “last great monetization” mindset: extract value from competitive hydrocarbon assets while the world still needs large volumes of oil, even as it prepares for an energy transition that will eventually reward flexibility, technology, low-carbon fuels, and logistics dominance over cartel discipline. The official UAE Energy Strategy 2050 aims to triple renewable contribution, raise installed clean energy capacity to 19.8 GW by 2030, improve energy efficiency by 42-45 percent, and mobilize AED 150–200 billion in investment by 2030. In parallel, the revised strategy envisions hydrogen production rising to 1.4 million tonnes annually by 2031, while Masdar has already reached 65 GW of global clean-energy capacity on its way to a 100 GW target by 2030. This is not the posture of a state retreating from energy; it is the posture of a state broadening what “energy power” means.

So what exactly is the triangle? In my reading, it is this: Saudi Arabia remains the old anchor of Gulf oil order; the United States remains the indispensable security guarantor and strategic access point; and China, together with BRICS and the wider Asian marketplace, represents the future pole of energy demand, infrastructure, technology, and alternative financial arrangements. The UAE is positioning itself not as a subordinate inside any one of these axes, but as a swing state among all three.

Its relationship with Riyadh is no longer one of quiet alignment alone. Reuters notes a widening rivalry between the UAE and Saudi Arabia, extending from oil policy to regional geopolitics and competition for capital, talent, and corporate headquarters. OPEC once helped discipline these differences inside a common framework. Outside OPEC, the UAE has more room to pursue sovereign economic interests without having to wrap them in the language of Gulf solidarity.

Its relationship with Washington, meanwhile, remains indispensable but increasingly transactional. The UAE is a major US partner and, as Reuters notes, has deepened its ties with Israel since the Abraham Accords, partly because that relationship offers another channel into Washington’s strategic ecosystem. Yet the Emirati calculation is not one of dependence; it is one of insurance. Leave OPEC, keep US security ties, retain Western capital access, and still preserve room to trade, invest, and coordinate with Asia.

And then there is China and the BRICS dimension. Officially, the UAE says its BRICS membership reflects a commitment to multipolar governance, diversified economic cooperation, and a stronger role in shaping global economic debate. Beijing, for its part, has called for deeper energy cooperation with the UAE not only in hydrocarbons but also in storage, hydrogen, and electric mobility. This is important: China is not just buying barrels; it is embedding itself in the next-generation energy ecosystem.

The de-dollarization angle should be handled with sobriety, not theatre. The dollar is not collapsing tomorrow, and the UAE is not leading an anti-American monetary revolt. But the evidence of hedging is real. India’s first crude payment to the UAE in rupees showed that local-currency settlement in energy trade is no longer merely theoretical. Separately, Reuters reported a yuan-settled LNG trade linked to ADNOC Trading, underscoring China’s steady effort to internationalize its currency in hydrocarbon transactions. These developments do not dethrone the petrodollar overnight, but they do chip away at its monopoly by normalizing optionality. That is the real story: not replacement, but redundancy.

In the immediate term, the market impact may be limited because the Strait of Hormuz crisis has distorted normal supply dynamics. Reuters notes that shipping constraints, not just production policy, are currently shaping the market. But once conditions stabilize, the longer-term implications could be significant: a structurally weaker OPEC, more competition for market share, and a more volatile pricing environment if quota discipline erodes further. In effect, Saudi Arabia may find itself more isolated as the system’s residual stabilizer.

For the broader Muslim world, the message is equally consequential. Gulf powers are no longer operating through a single bloc logic. They are pursuing issue-based, interest-driven alignments, with the West on security, with Asia on commerce, with BRICS on institutional reform, and with climate diplomacy on future legitimacy. States that still read the region through the old binaries of “pro-West” versus “anti-West” will misunderstand the moment. The new Gulf diplomacy is hybrid, layered, and unapologetically selective

For Pakistan, this is not a distant Gulf story. It goes directly to energy security, remittances, trade, and diplomatic calibration. The UAE remains one of Pakistan’s most important economic partners; State Bank of Pakistan data for October 2025 showed remittances from the UAE at $697.7 million, second only to Saudi Arabia. Pakistan, therefore, has a direct stake in the stability, prosperity, and strategic direction of the Emirates.

Islamabad should draw three lessons. First, do not treat the Gulf as politically static. The UAE is no longer merely a rentier state selling oil under a collective banner; it is becoming a logistics, finance, technology, renewables, and strategic capital hub guided by the “We the UAE 2031” vision, which aims to double GDP to AED 3 trillion, raise non-oil exports to AED 800 billion, and expand foreign trade to AED 4 trillion. Second, Pakistan should quietly study selective local-currency and payment-link experiments in regional trade, not as ideological gestures but as tools for reducing transaction costs and external vulnerability. Third, Pakistan must pitch itself to the UAE not only as a labour exporter or aid seeker, but as a serious partner in food security, port connectivity, refinery capacity, petrochemicals, renewables, digital infrastructure, and corridor economics.

The “love triangle” metaphor is effective because it recognizes something policymakers often resist admitting: power today belongs to those who can stay central to multiple systems at once. By leaving OPEC, the UAE is signaling that it wants freedom to produce more oil, trade more flexibly, diversify faster, and negotiate from a position no longer defined by cartel discipline alone. This is not the end of Gulf influence; it may be the beginning of a more fluid and sophisticated phase of it.

For Pakistani readers and policymakers, the takeaway is clear. The future will not be shaped by choosing one camp and denouncing the rest. It will be shaped by strategic dexterity, institutional competence, and the ability to engage a multipolar world without losing policy coherence at home. In that sense, the triangle is not just Abu Dhabi’s story. It is a warning, and an opportunity, for all states that still imagine the old order will return by habit. It will not.

The author is a Cybersecurity & Digital Policy Expert with 25+ years of progressive experience in managing enterprise-wide digital operations,

cybersecurity frameworks and risk management across military, Government, and International environments. Project management professional and CISSP-certified security professional with proven expertise in financial systems protection. Demonstrated success in leading digital transformation initiatives, implementing robust security protocols, and ensuring regulatory compliance in high-stakes environments. Currently, He is part of Governance, Risk, and Cybersecurity at AXI Technologies in Islamabad.

{kind=link}

{kind=link}